This month, you asked us: Where do you find that most businesses are under-insured? And why do you think they are?

The answer: Business Interruption + Cyber Liability.

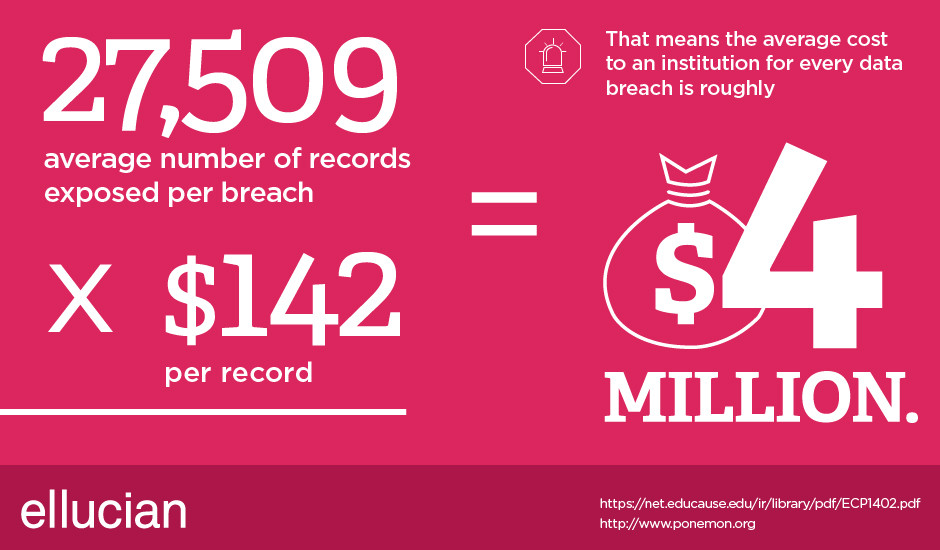

Why? Yes, you do need it–and you really can afford it. Most small to midsize companies pass on these coverages because of added cost and a misunderstanding or underestimation of their need or risk. But consider this: Business Interruption and Cyber attacks are common, and can be financially crippling. Nearly four out of five — 78% — organizations experienced some sort of data breach in the past two years, and 71% of them failed because of it. Read our advice below on why it’s essential and why it really won’t cost you that much.

:|: Yes, you need Cyber Liability insurance. Target. Anthem. Sony. It seems that every week, a new story hits the media about a major hack. If you’re a small business owner, you may wonder: What would I if something like this were to happen to my company? How can I protect myself? Do I need cyber insurance?

The internet has made everyone vulnerable, the costs to fix an intrusion are very expensive, and coverage is inexpensive (in comparison), so it’s silly to take a risk. If you are a retailer that accepts credit card payments, you are open to cyber liability risk. Even if you don’t, you probably have personal information from your employees and/or customers, and perhaps intellectual property from vendors.

What does the coverage buy you? It pays for out-of-pocket expenses after a breach, remediation costs, cost to notify impacted people, credit monitoring for those impacted, and identity theft resolution services should a theft occur. It can also cover public relations.

:|: Yes, you need Business Interruption insurance. Business interruption is likely to happen at some point during the lifetime of your business. The rising number of natural disasters (increasing from 400 to 600 major incidents annually, according to a recent survey from global insurer Allianz), makes this likelihood even greater.

Business Interruption is a very misunderstood coverage area. Most business owners assume that their standard Property policy covers them from loss. However, most standard Property policies cover only loss or damage to tangible items (i.e. equipment and inventory and your warehouse, office, or store), not lost profits if your business cannot operate (which an Interruption policy would cover).

Also, consider that your business is at risk when related businesses are affected by disaster. For instance, a fire at your credit card server’s processing center could take down your ability to accept payment, or flooding or a strike at a key manufacturing or delivery center could cause disruption to your supply chain. These events hurt your finances even though your facility may be undamaged. “Contingent business” insurance covers your lost profits in these disaster scenarios.

According to the Federal Government, statistics show that of all businesses involved in a major loss, 43% never trade again and 28% fail over the next three years. This statistic means only 29% survive and 71% fail following a business interruption event.

What does the coverage buy you? A Business Interruption policy covers lost revenue if your business has to temporarily shut down due to a disaster (whether to the supply chain or the business directly), payroll for your employees, expenses (i.e. electricity) and other costs while you’re preparing to reopen, and can be the deciding factor in whether your business thrives or fails.

Case In Point: Consider a disaster like Hurricane Sandy. Property policies cover damage to the structure and equipment listed on affected business policies (a good reminder as to why it’s so important to update your policy when you expand, purchase new equipment, etc.), but do NOT cover revenue lost while repairs were made or businesses found new locations. Businesses not covered by an Interruption policy would have to pay out of pocket to cover bills like mortgage and utilities (that do not quit following a disaster), employee payroll (or risk losing valuable, trained employees), and for temporary relocation during a rebuild. Covered businesses would have these expenses covered by their insurer.

How Much Do You Need? Calculating coverage needs and business worth is also a barrier to many companies. When there is a lack of understanding of the coverage, it is difficult for a business to set values to its worth, which is necessary to ensure the right coverage amount. For example, a study from the Chartered Institute of Loss Adjusters (CILA) in 2012 shows that 40% of all companies have declared values that are too low, and by as much as 45%!

To figure out your ideal coverage amount, you should envision how your business would be affected by a catastrophe (hurricane, fire, etc.). Consider all costs that you would continue to pay even if your business couldn’t operate (loan or lease payments and taxes). You may also need to keep workers on the payroll while you rebuild, so your insurance should reimburse you for their salaries.

:|: The Cost? You’ll pay less for it than you’d expect. How much you need is dependent on the size of your business, your company’s balance sheet (for Business Interruption), and the type and amount of data your company manages (for Cyber Liability). A rider on a standard insurance policy may be sufficient for small companies, provided you do not process or store a large amount of sensitive information.

If a rider is sufficient for your business, Cyber Liability insurance can cost as little as $45 to $75 a year for $10,000 to $20,000 of coverage. Adding business interruption coverage and network security liability coverage could cost in the low hundreds per year. If you need a stand-alone policy, your premium cost will generally be at least $500, but more typically $750 and above. For larger businesses, this goes up, depending on the type of coverage you need.

:|: The Summary: Cyber Liability and Business Interruption are not part of your standard business insurance policy. Even if your policy has small amounts of these coverages as an enhancement, the amount of protection is not enough to really protect you.

- Business Interruption insurance can be the difference between staying in business or disappearing after a direct loss (i.e. fire, flood), or an indirect loss (i.e. your credit card server goes down for a day, your distributor isn’t able to make a delivery crucial to your business).

- Cyber coverage is too often built into another coverage on a policy, diluting the limits and reducing coverage. If your businesses uses a credit card vendor to accept payment or collects email addresses for a newsletter, you are open to cyber exposure – and should have a stand alone policy to protect your business and the costs that it could incur should your credit card vendor go offline, making you unable to accept payment (and therefore losing hours or days of income), or a hacker should steal your marketing lists or other Personally Identifiable Information about your clients.

Our advice: General coverage often isn’t enough to protect your business. Passing on these two added coverages can strike a fatal financial blow to your business.

Business Interruption and Cyber Liability are added protections your insurance company can tailor to the risks in your specific line of business. Believe us, your risk of the costs following a major loss (like a hack or business interruption) far outweigh the low cost of upfront premium coverage.

Our goal is to help you avoid costly pitfalls associated with cyber or interruption breaches, and make sure that the financial health of your business is protected against accidents or catastrophes. Give us a call to review your policy and add the coverage you need.